I've been trading in the Indian Stock Markets for over eight years. Like many beginners, I initially lacked a specific system or strategy for buying and selling stocks. My decisions were often based on recommendations from friends, analysts, and news sources. Unsurprisingly, this approach didn't yield substantial gains. Without a consistent system, I lacked conviction in my trades.

To change this, I decided to develop a time-tested, back-tested strategy that would allow me to trade based on signals, eliminating emotional biases. This led me to explore momentum strategy trading. I first encountered the basics of this strategy in a Zerodha module, which inspired me to backtest the system using data from 2014 onwards to see if it had worked in the past.

Data Collection and Preparation

I began by downloading the end-of-day (EOD) data for all stocks in the NIFTY500 universe for the specified time frame. It's important to note that the index constituents change very often (twice in a year), so I had to ensure I was using the correct set of stocks for each month of the backtesting period. Failing to do this and using only the current universe would introduce significant survivorship bias, skewing the backtest results.

Backtesting the Momentum Strategy

With the EOD data spanning the last 10 years in hand, I wrote the backtesting algorithm. The strategy itself, in its most basic form, is straightforward:

- Monthly Stock Selection: At the beginning of each month, identify the stocks that have shown the highest percentage price movement over the past year. Rank these stocks in descending order of their price changes and select the top 30 performers.

- Capital Allocation: Allocate equal capital to these selected stocks and purchase them at the start of the month.

- Hold Period: Hold these stocks for the entire month, taking no action until the beginning of the next month.

- Monthly Recalculation: At the start of the following month, repeat the stock selection process, incorporating data from the previous month and excluding data from the earliest month.

- Portfolio Adjustment: Sell any stocks from the previous month's list that no longer appear in the new top 30 list and buy the new stocks that have entered the top 30.

This method ensures that we continuously hold stocks demonstrating strong momentum while discarding those that no longer exhibit momentum. The process is repeated at the start of each month.

Results and Performance Analysis

What I have described above is perhaps one of the simplest forms of constructing a momentum portfolio. I backtested this strategy from 2014 to 2023, and here are the results:

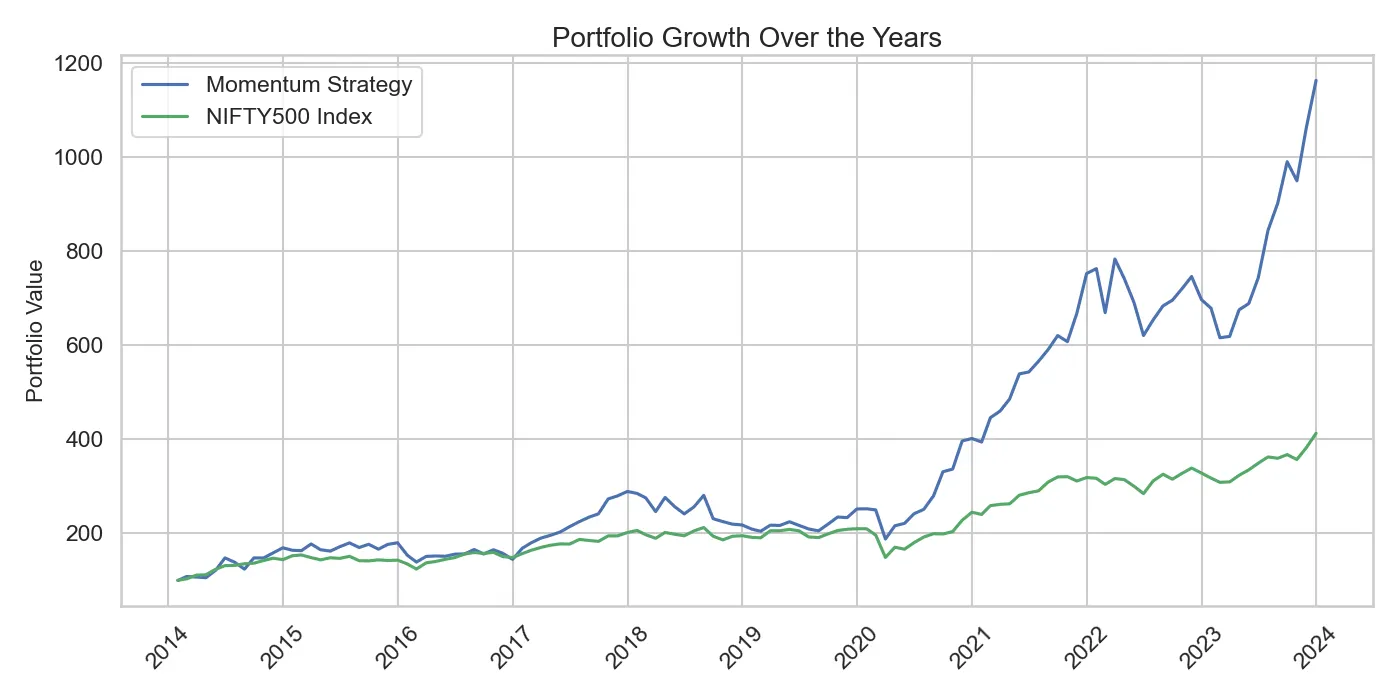

The graph above compares the growth of a portfolio using the simple momentum strategy described earlier against a buy-and-hold approach with the NIFTY500 index from 2014 to 2024. Except on a few occasions, the momentum strategy has consistently outperformed the benchmark index. This strategy has performed exceptionally well in trending markets, such as in 2017 and the period following the pandemic. While both the strategy and the index have shown growth during these times, the momentum portfolio has significantly outpaced the index, demonstrating its ability to capture the best-performing stocks and capitalise on upward trends.

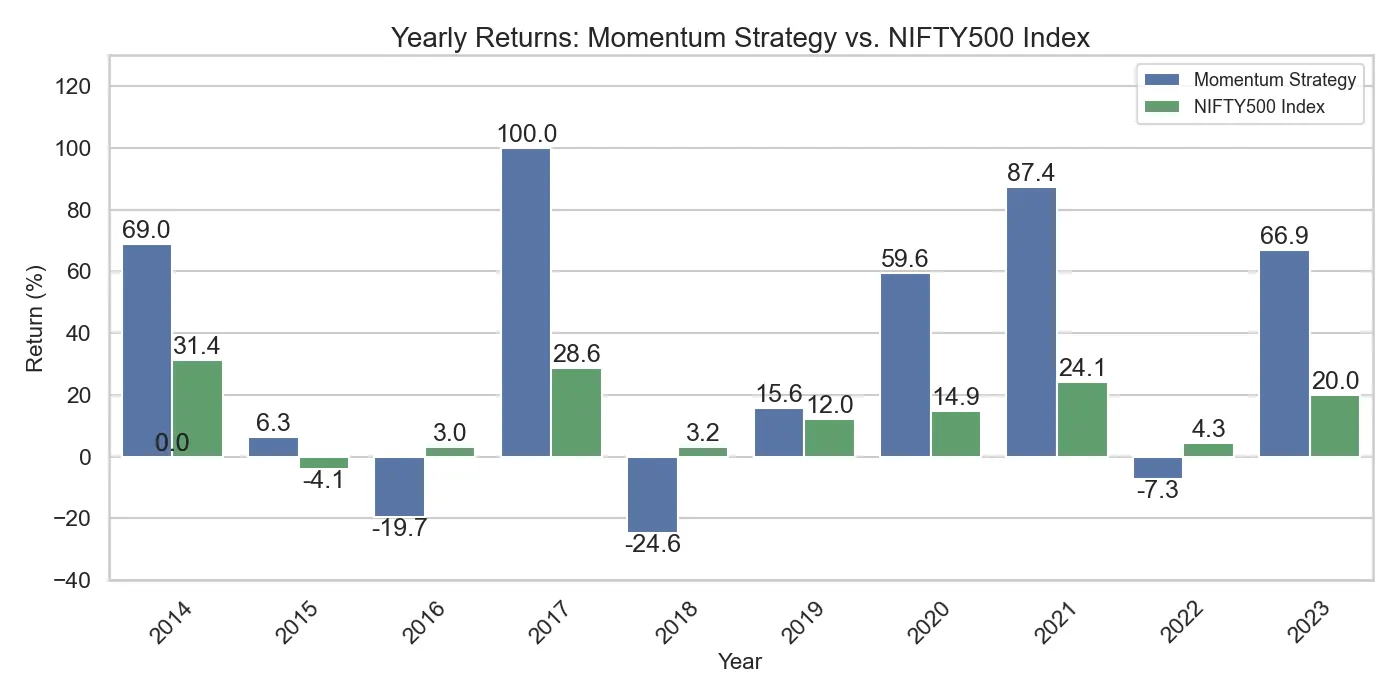

Following the analysis of the portfolio equity curve, I now present a bar graph comparing the yearly returns of the momentum strategy against the NIFTY500 index from 2014 to 2023. The momentum strategy has shown significant outperformance in years such as 2014, 2017, 2020, 2021, and 2023. For instance, in 2017, the strategy achieved a 100% return compared to the NIFTY500's 28.6%. In volatile market years such as 2020 and the post-pandemic period, the momentum strategy not only held its ground but also provided substantial returns, significantly outperforming the index.

However, it's important to note that during non-trending and sideways markets like 2016, 2018, and 2022, the strategy underperformed the NIFTY500 index. While the index experienced insignificant growth during these years, the momentum strategy faced steeper losses, with returns of -19.7% in 2016 and -24.6% in 2018. This highlights a limitation of the momentum strategy in bearish or choppy markets.

Drawdowns and Risk Analysis

Now, let's explore the downsides of the strategy by looking at the drawdown curve:

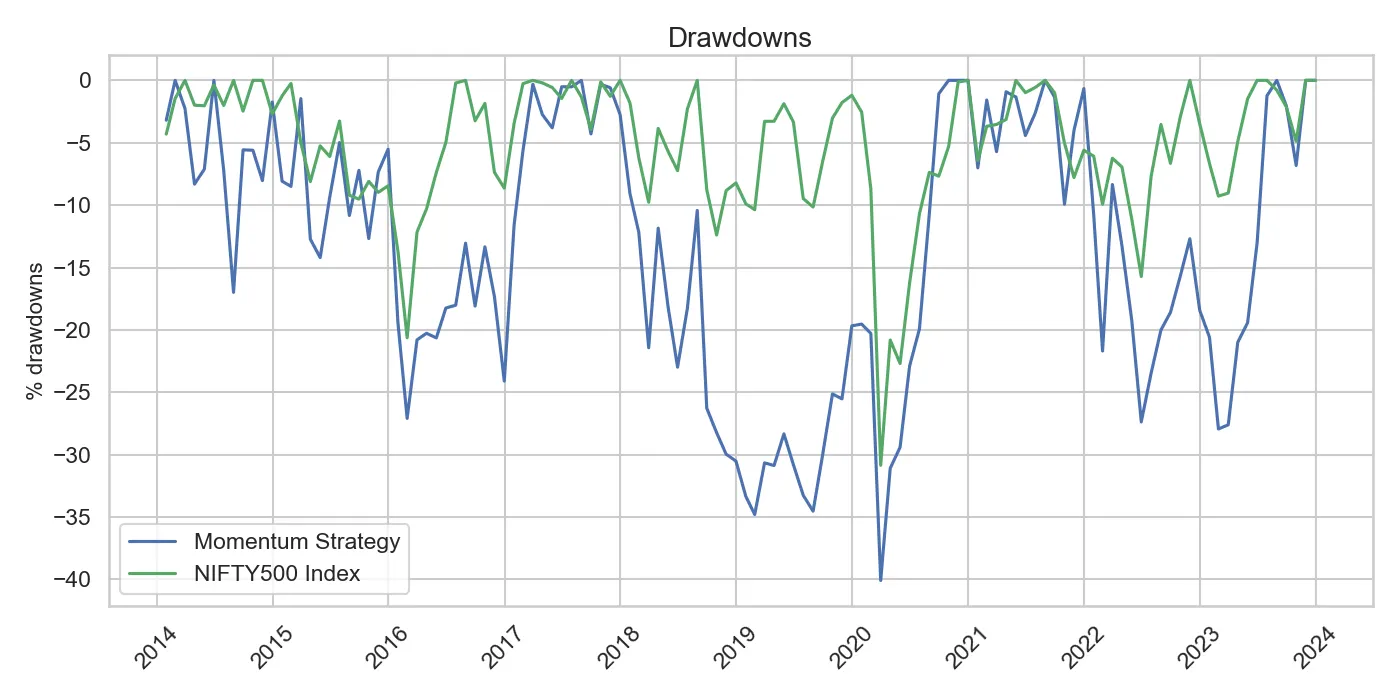

The drawdown curve above highlights the higher volatility and risk associated with the momentum strategy compared to the NIFTY500 index. The momentum strategy experiences deeper and more frequent drawdowns, particularly during bearish and choppy market phases like in 2016, 2018, 2020, and 2022, where drawdowns approached nearly -40%. These significant declines underscore the strategy's vulnerability in declining markets.

Key Performance Metrics

Finally, let's summarise the overall performance of the strategy by looking at few important metrics. The summary table below compares the key performance metrics of the momentum strategy against the NIFTY500 index:

| Metric | Momentum Strategy | NIFTY500 Index |

|---|---|---|

| CAGR (%) | 27.8 | 14.8 |

| Max drawdown (%) | -46.2 | -38.3 |

| Max drawdown duration (days) | 647 | 352 |

| Avg. monthly return (%) | 2.39 | 1.32 |

| % positive months | 61.6 | 62.5 |

| Best month return (%) | 21.9 | 14.5 |

| Worst month return (%) | -24.8 | -24.4 |

| Monthly volatility (%) | 7.9 | 4.9 |

The summary statistics table highlights the strengths and weaknesses of the momentum strategy compared to the NIFTY500 index. With a CAGR of 27.8%, the momentum strategy significantly outperforms the index's 14.8%, demonstrating superior long-term growth. However, this higher return comes with increased risk, as evidenced by a maximum drawdown of -46.2% and longer recovery periods. The strategy's higher average monthly return of 2.39% suggests better month-to-month performance, despite having slightly fewer positive months than the index. The momentum strategy also exhibits greater monthly volatility, reflecting its more aggressive approach.

Conclusion

Momentum trading offers significant rewards, but it also comes with its own set of risks. By understanding these dynamics, traders can better navigate the markets and potentially enhance their returns. However, this is just the beginning of our exploration into momentum strategies. There are many intriguing questions and directions one can pursue to build an even more refined momentum-based strategy:

- Stock Universe: What happens if we change our stock universe from NIFTY500 to something else like NIFTY200, all stocks above 1000 crores in market cap, or some other criteria to filter down the list?

- Portfolio Size: What if we choose a different number of stocks in the portfolio instead of 30? What happens with only the top 10 or top 5 stocks? What if we increase it further to the top 50?

- Ranking Criteria: Is there another way to rank the stocks apart from percentage change in prices? Shouldn't we also take volatility into account?

- Momentum Persistence: The momentum formation is considered over the past year. It's possible that some stocks appearing in the top 30 list might have lost some momentum in the final months/weeks but still continue to exist in the list because of their earlier significant moves. What if we start filtering out stocks that don't show persistent momentum at the end of the formation period?

- Stop Losses: What happens if we start putting stock-wise stop losses? Do we have anything to gain if we remove the stocks once they go down by 10%? 20%?

These are just a few of the many questions worth evaluating. I have already conducted analyses for some of these scenarios and will publish the results soon. Stay tuned for more insights and findings!

Credits: Nobal Dhruw